Financial fraud is advancing faster than ever, driven by real-time digital payments, automated attacks, and criminals using tools like Generative AI to create highly convincing scams. With global digital transactions expected to exceed $33 trillion in 5 years, banks and financial institutions are under immense pressure to protect customers and maintain trust.

However, traditional fraud detection systems can’t keep up. They react too slowly, require constant manual updates, and often misidentify genuine customers as fraud risks, creating costly friction and operational strain.

Machine learning is changing this landscape. By analyzing massive amounts of data in real time and continuously learning from new fraud behaviors, ML transforms fraud detection into a proactive, adaptive defense system. It helps institutions reduce false positives, detect emerging threats earlier, and build stronger, smarter protection across all financial channels.

In this post, we will discuss the changing landscape of financial crime, how to use machine learning, the types of fraud-detection algorithms, and where experts can help.

The Complexity of Financial Crime

To understand the power of ML in fraud detection, we must first look at the complexity of the current fraud landscape. Financial crime is not just one act; it’s a wide range of illicit activities designed to exploit vulnerabilities in the financial ecosystem.

Common Types of Financial Fraud

The most persistent and damaging types of fraud include:

- Payment Fraud: Unauthorized transactions on credit cards, debit cards, and digital wallets, often using stolen or fake identities.

- Identity Fraud: Creating completely fabricated identities (synthetic identities) by combining real and fake data to open new accounts or lines of credit.

- Account Takeover (ATO) Fraud: Criminals gaining unauthorized access to a customer’s existing account (e.g., through credential stuffing) and using it to initiate high-value transfers.

- Loan and Application Fraud: Providing false income or employment information to secure financing.

- Money Laundering: Sophisticated structuring and layering of illicit funds to hide their criminal origin.

Why Traditional Fraud Detection Systems Don’t Work

Older fraud prevention systems rely on human analysts writing specific, fixed rules. For example, a rule might be: “Stop any transfer over $5,000 made outside the customer’s home country.” This fixed approach has three major weaknesses:

- Stagnation (Concept Drift): Rules are static and require manual updates. Fraudsters, however, change their methods in days or hours, a phenomenon known as concept drift.

- High False Positives: Legitimate customer behavior changes frequently. When a good transaction violates a rule, it creates friction, frustrating the customer.

- Lack of Context: They cannot simultaneously evaluate thousands of behavioral, transactional, and device-level variables to understand the full risk picture.

How Machine Learning Helps in Fraud Detection in Banking

AI and ML solve the problems of old systems by using complex pattern recognition to spot fraud where no human-defined rule exists.

-

Learning and Adapting Automatically

Unlike fixed rules, ML models, especially those that use continuous learning, automatically adjust and improve their judgment as they process new data. This adaptive learning means the models evolve with new fraud patterns, effectively stopping concept drift and ensuring the system always fights the latest tactics.

-

Fast, Real-Time Decisions and Scale

Modern ML models are designed for high-speed, instant scoring. This means they can analyze millions of transactions per second, providing a real-time fraud detection decision in milliseconds, fast enough to block a fraudulent transaction before it is authorized. This level of speed and scalability is critical for digital banks that handle massive transaction volumes.

-

Finding Hidden Clues

The biggest advantage is the ability to find complex patterns that are simply invisible to human analysts or simple rules. ML models can link together thousands of clues, from the velocity of new account applications to subtle changes in a user’s keystroke behavior, to create highly accurate risk scores.

Also Read: AI in AML

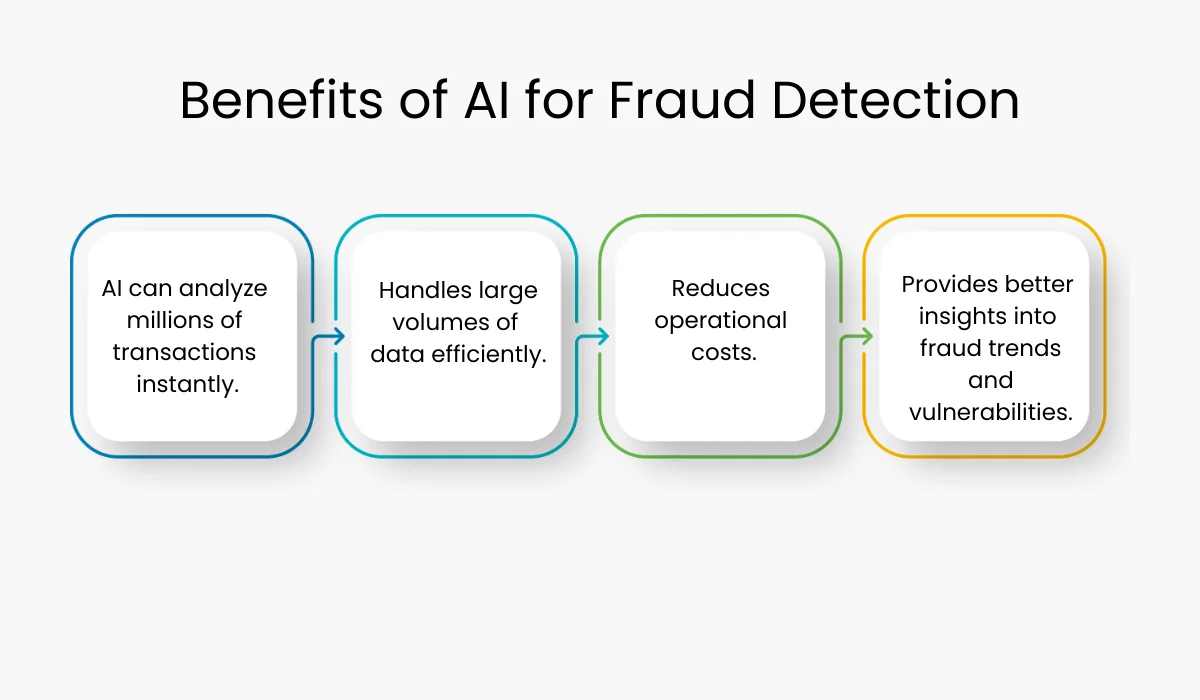

Benefits of Using AI for Fraud Detection in Banking

Machine learning models offer several crucial advantages over legacy systems, providing institutions with a superior defense mechanism:

1. Drastically Reduced False Positives

The biggest operational win for AI systems is their precision. Unlike rule-based systems that use rigid thresholds (e.g., “flag all transactions over $5,000”), ML analyzes hundreds of behavioral data points simultaneously (location, device, time, typical spending habits). This sophisticated context allows AI to accurately distinguish between a high-value legitimate transaction and genuine fraud, leading to far fewer false positives. This reduces customer friction and saves banks millions in manual investigation costs.

2. Real-Time, Instantaneous Decision Making

In the world of high-speed digital payments, transactions happen in milliseconds. AI-powered models can score the risk of a transaction instantaneously as it occurs, allowing financial institutions to approve, deny, or flag a payment before it is finalized. This capability is critical for preventing losses in real-time, especially in high-volume environments like credit card processing and wire transfers.

3. Detection of Novel and Zero-Day Fraud

Criminal techniques are constantly changing, especially with the use of Generative AI to scale attacks. Traditional systems fail because they only catch what they’ve been explicitly programmed to find. Machine learning, however, is trained to identify anomalies, deviations from normal behavior. This inherent capability allows AI models to automatically detect completely new or “zero-day” fraud schemes without requiring manual updates or new rules from a human analyst.

4. Scalability and Handling Massive Data

As global digital transactions surge toward the multi-trillion-dollar mark, human teams and rule systems simply cannot process the volume. AI systems are infinitely scalable, capable of processing and learning from billions of data points (transactions, logins, device data, application forms) across all channels simultaneously. This provides a unified, highly effective view of risk across the entire institution.

Type of Fraud Detection Algorithms

Building an effective system requires deploying different types of fraud detection algorithms. These are primarily divided into three groups: Supervised, Unsupervised, and Deep Learning.

1. Supervised Learning

This is the most common technique used in mature fraud systems. Supervised models are trained on historical data in which each transaction is clearly labeled as either ‘Legitimate’ or ‘Fraudulent’.

- Most Common Technique: The most common machine learning technique for high-precision results is Gradient Boosting Machines (GBM), such as XGBoost, which excel at classification tasks.

- Use Case: Predicting known types of fraud, like credit card misuse, where clear historical patterns exist.

2. Unsupervised Learning

Since criminals constantly innovate, a model trained only on past fraud will miss future fraud. This is why unsupervised learning is essential. These algorithms work with unlabeled data, focusing on Anomaly Detection, finding data points that are significantly different from what the model considers “normal” behavior.

- How it Works: Algorithms like Isolation Forest or clustering techniques are key. This is the primary fraud detection using a machine learning approach for discovering brand-new threats.

- Use Case: Detecting novel or “zero-day” fraud schemes that have not yet been labeled by human analysts, such as sudden, coordinated attacks targeting a system weakness.

3. Deep Learning and Hybrid Models

Deep Learning uses complex neural networks to automatically extract features and recognize patterns from complex data.

- Key Use: Recurrent Neural Networks (RNNs) or Long Short-Term Memory (LSTM) networks are highly effective for sequential data analysis. They track complex user behavior over time, recognizing subtle deviations in a sequence of events (e.g., a sudden change in steps before a fraudulent wire transfer).

- Hybrid Approach: The most successful contemporary fraud systems combine these methods. For example, an unsupervised model flags an anomaly, which a high-precision supervised model then scores for the final decision.

Also Read: Implementing AI in Fintech? Avoid These 7 Biggest Mistakes!

Setting up a successful ML-based fraud detection system is a systematic process requiring expertise in data science, engineering, and financial risk. Follow these steps for implementation:

Step 1: Data Collection & Integration

Gather high-quality, diverse data streams, including transaction details, user login history, device fingerprinting (IP address, browser type), and geolocation data.

Step 2: Creating Smart Features (Feature Engineering)

Transform raw data into meaningful clues. This is critical for model success. Effective features often include:

- Velocity Checks: How many transactions has this user made in the last 10 minutes/hour/day?

- Behavioral Norms: Is the current transaction statistically unusual for this user’s history?

- Network Links: Is this device connected to any known fraudulent accounts?

Step 3: Dealing with Unbalanced Data

Because fraud is rare (often <0.1% of transactions), models must be trained using techniques like:

- Oversampling (SMOTE): Creating synthetic, realistic fraud examples.

- Cost-Sensitive Learning: Telling the model that missing a real fraud case (a false negative) is much worse than stopping a good transaction by mistake (a false positive).

Step 4: Model Testing and Checking

Models must be rigorously validated against the institution’s risk appetite. Key metrics include:

- Precision: How many flagged transactions were actually fraud? (Impacts false positives).

- Recall: How many real fraud cases did the model catch? (Impacts fraud losses).

Step 5: Going Live and Scoring in Real-Time

The model must be deployed to a production environment using APIs and streaming frameworks (such as Kafka and Spark) to score transactions in under 100 milliseconds and feed immediate actions back into the processing system.

How an ML Development Company Can Help

The journey to building a fully adaptive, real-time machine learning-based fraud detection system is complex and requires specialized expertise. Specialized ML development companies provide the necessary support:

- Custom Solutions: They design models specifically tailored to an institution’s unique transaction patterns and risk tolerance.

- Seamless Integration: They ensure deployment into existing core banking and payment processing systems.

- Compliance & Security: They build systems with XAI embedded by design, ensuring adherence to strict regulatory standards.

- Continuous Optimization: They manage ongoing maintenance, retraining, and model updates to ensure the system remains effective as the fraud landscape evolves.

Conclusion

The speed of the modern digital world has rendered traditional fraud defenses obsolete. Machine learning for fraud detection is the essential adaptive technology required to protect financial assets, safeguard customer trust, and ensure regulatory compliance in the 21st century. By effectively leveraging supervised, unsupervised, and advanced hybrid techniques, supported by the clear logic of XAI, financial institutions can finally gain the upper hand against criminals.

The time to upgrade your defense infrastructure is now. Partner with a machine learning app development company to transform your institution’s risk management posture from a cost center into a strategic advantage.