According to the Research and Markets AI in FinTech Global Report 2026, the market size for artificial intelligence in the fintech industry has jumped to 23.05 billion dollars this year, growing at an annual rate of over 30%. This data highlights a deeper operational reality: fintech platforms are no longer just using AI to predict outcomes. They are trusting it to take action.

This transition into autonomous and conversational operations means software platforms can now run compliance checks, route massive corporate payments, and write initial lending agreements with minimal human intervention.

If you are operating a financial platform or building digital workflows, understanding the use cases of AI in fintech is the best way to keep your operations modern and secure.

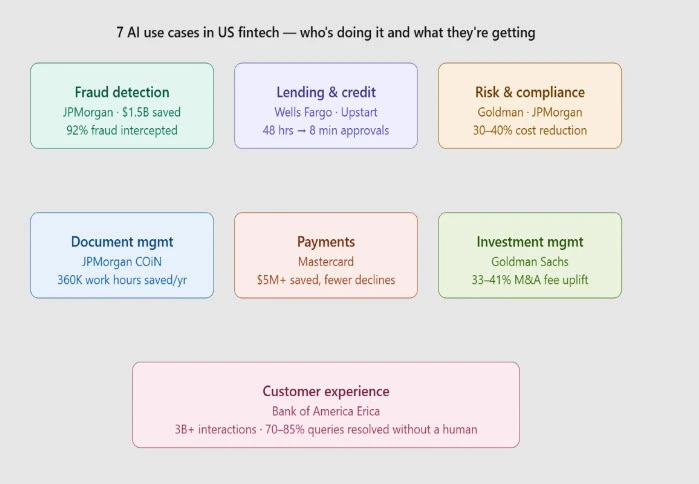

- JPMorgan Chase saved nearly $1.5 billion through AI across fraud detection, trading, and credit decisions and its COiN platform saves over 360,000 legal work hours every single year by automating contract review.

- AI is stopping 92% of fraudulent transactions before they go through, that’s the single clearest ROI case in banking right now (ABA Banking Journal, January 2026).

- Loan approvals that used to take 48 hours now take 8 minutes at institutions running AI-powered underwriting.

- Bank of America’s Erica has had over 3 billion customer conversations, handling 70–85% of routine queries without a human agent ever getting involved.

- 42% of card issuers using Mastercard’s AI fraud tools saved more than $5 million in fraud losses over just two years.

- The AI in the fintech market hit $17.79 billion in 2025 , up 25% from the year before, with fraud detection and customer AI leading the way.

Where Are Fintech Companies Actually Using AI?

Fraud Detection: The Clearest Win in Banking Right Now

If you want to understand where AI delivers the most immediate, measurable value in banking, fraud detection is your answer. And the data makes it hard to argue otherwise.

AI systems are now intercepting 92% of fraudulent transactions before they are approved, according to the ABA Banking Journal. A year ago that number would have seemed ambitious. Now it’s table stakes at leading institutions.

This is why AI in fraud detection continues to be one of the fastest-growing investments in financial services. Unlike traditional rule-based systems, machine learning models continuously adapt to new fraud patterns, helping institutions reduce false positives while strengthening fraud prevention efforts.

- Identity verification and authentication

About 70% of fintech logins now use biometric authentication backed by AI liveness detection which is increasingly necessary, given that dark web trading of AI-generated deepfake kits jumped 223% in 2024.

- Anti-Money Laundering (AML) monitoring

On the AML side, AI can map transaction networks and catch structuring patterns across thousands of accounts simultaneously, work that used to require armies of compliance analysts. Leading institutions have cut AML compliance overhead by 30–40% as a result, according to Trantor’s 2026 analysis.

Lending and Credit: From Two Days to Eight Minutes

The change in lending is hard to overstate. Getting a loan approved used to take 48 hours. A loan officer would manually review tax returns, bank statements, pay stubs, calculate debt-to-income ratio, and make a call. AI-powered underwriting does all of that in under 10 minutes.

What’s happening underneath is fairly simple to understand:

- AI reads and interprets financial documents the same way a loan officer does, just faster and without fatigue.

- It flags inconsistencies, calculates risk metrics, and produces a recommendation that feeds directly into the decision.

- The loan officer’s judgment is still there in how the model was trained, it’s just no longer waiting on their calendar.

Upstart, a loan lending company based in California, has built its entire business around this model. Their ML-based underwriting consistently produces lower default rates than traditional lenders, not because the AI is smarter, but because it can assess creditworthiness across a broader and more accurate picture of someone’s financial life.

Risk and Compliance: The Quiet Cost Saver

Nobody puts “compliance automation” in a press release. But it’s one of the highest-ROI AI applications in financial services, and the window for getting ahead of it is closing fast.

What AI actually does here:

It monitors regulatory changes, flags policy gaps, updates compliance documentation, and generates audit-ready reports that used to consume entire compliance departments.

Goldman Sachs and JPMorgan both use AI for risk management, modeling portfolio exposure and stress scenarios dynamically from historical price data, options chains, and macro signals.

However, one of the biggest challenges associated with AI compliance automation is balancing innovation with regulatory accountability. Financial institutions increasingly need governance frameworks that ensure explainability, maintain human oversight, and support audit readiness.Document Management: 360,000 Hours a Year

JPMorgan’s COiN platform is the one of the most cited examples of AI in document management. IT reviews 12,000 commercial credit agreements in seconds and saves the bank over 360,000 legal work hours annually. Tasks that previously required a team of lawyers working for weeks now happen before a cup of coffee goes cold.

Beyond contract review, the everyday productivity gains from AI-powered document management compound across the organization. Compliance officers who used to spend hours hunting through internal policy libraries to answer a question about a product feature can now get accurate answers in seconds.

Loan applications, insurance claims, audit reports. AI extracts the key data from all, generates summaries, and routes everything to the right team without anyone touching it manually.

Payments: Fewer Fraud Losses, Fewer Declined Cards

Mastercard’s 2026 research found that 42% of card issuers and 26% of acquirers saved over $5 million in fraud losses over two years using AI. That’s one metric. Here’s the one that gets less attention: 83% of industry leaders said AI reduced false positives in payment authorization.

False positives, legitimate transactions that get declined, are a bigger commercial problem than most people realize.

A customer whose card gets declined at checkout because an algorithm didn’t like the merchant category doesn’t just call to complain. They often switch cards. AI that learns to distinguish a real fraud pattern from an unusual-but-legitimate transaction doesn’t just save on fraud losses; it keeps customers from churning.

Intelligent payment routing adds another layer. AI selects the optimal payment network for each transaction based on cost, speed, and success probability. For high-volume processors, even a small improvement in routing efficiency adds up to serious money.

Investment Banking: AI Is Doing the Research

Many of the most advanced examples of generative AI in fintech are concentrated in investment banking and knowledge-intensive functions. Rather than replacing analysts, these systems accelerate research, summarize large volumes of information, and improve decision-making speed across complex workflows.

Goldman Sachs has deployed an internal AI assistant across its knowledge workers and is projecting a 33–41% productivity uplift in M&A advisory fee revenue. To be clear about what that means, analysts can now synthesize earnings reports, regulatory filings, competitor analyses, and market data in the time it used to take to read one document.

JPMorgan has 450+ AI use cases in the fintech industry alone, running across origination, capital markets, and operations. Over 200,000 internal users are on the platform. The bank has spent $2 billion on AI since 2023, per Whitehat SEO’s April 2026 analysis of investment banking AI adoption. Pitch books still get made, due diligence still gets done, it just takes a lot less time.

Customer Experience: The Front Door Has Changed

Three billion. That’s how many conversations Bank of America’s Erica has had with customers. It handles 70–85% of routine queries, from balance checks, transaction disputes, spending breakdowns, to product questions, without a human agent ever being needed.

The commercial logic is obvious: lower cost per interaction, 24/7 availability, faster resolution. But the part that often gets missed is what this has done to customer expectations. People who get an instant, accurate answer from Erica at 11pm aren’t going to be patient with a 20-minute hold time somewhere else.

Conversational banking AI has matured enough that it’s no longer a “nice to have.” The question has shifted from can we deploy this to how do we design the handoff to a human for the moments that actually need one.

How Much Should Banks Actually Invest in AI in 2026?

JPMorgan earmarked $20 billion of its 2026 technology budget for technology investments, with AI taking a substantial share. That’s a useful context but not a useful benchmark for most institutions.

What is useful:

IDC’s research found that organizations see an average 2.3x return on agentic AI investments within 13 months. McKinsey estimates AI could reduce certain banking cost categories by up to 70%, though a realistic net benefit, after technology costs, is more like 15–20%. McKinsey also projects a 4% return-on-tangible-equity advantage for AI-first banks over slower movers. That gap compounds over time.

The honest advice here isn’t about how much to spend. It’s about where to start.

The institutions seeing the strongest returns from artificial intelligence in financial services are prioritizing specific business problems rather than pursuing AI adoption for its own sake. Fraud prevention, document automation, and customer service optimization often deliver the fastest value because outcomes can be measured against existing operational benchmarks.

Where AI in FIntech Delivers the Most ROI?

Not all AI applications in financial services deliver the same value. Fraud detection and document automation typically generate measurable returns within the first few months due to immediate reductions in fraud losses and manual effort.

More complex use cases, such as AI-powered lending and underwriting, often take longer to validate but can drive substantial long-term business impact through improved risk assessment and operational efficiency.

How Softude Helps in Implementing AI in Banking and Finance

Building and deploying reliable, secure artificial intelligence systems in a heavily regulated financial environment requires deep technical expertise and strong domain knowledge.

You cannot rely on generic, out-of-the-box software models when dealing with sensitive user data, strict compliance audits, and real-time transaction flows.

Softude specializes in engineering custom AI solutions for banking and financial services that integrate smoothly with your existing financial technology infrastructure.

Our engineering teams understand how to build robust data guardrails, construct secure machine learning pipelines, and deploy explainable AI models that stand up to regulatory scrutiny.

If you are working through where AI fits in your roadmap, whether that’s fraud, lending, compliance, or somewhere else, we’d be glad to think it through with you. No pitch. Just a practical conversation.

Conclusion

Artificial intelligence in fintech has grown into the operational foundation. This shift means that market competitiveness is no longer defined just by digital features, but by how intelligently you automate your core data flows.

As automated systems handle more high-stakes decisions around credit, payments, and compliance, success requires a balanced approach. Fintech institutions must find a healthy middle ground: leveraging the immense speed and efficiency of automation while building clear human oversight and robust governance frameworks to keep financial workflows completely safe, accurate, and fair.

FAQs

Fraud detection, credit underwriting, compliance automation, document processing, and customer-facing virtual assistants are some of the areas where AI is used in the fintech industry.

Unlike traditional software that simply follows static rules, AI agents are autonomous software systems designed to execute complete workflows end-to-end. In fintech, an agent can look up a billing anomaly across multiple internal databases, write a plain-language summary of the issue, and route the case directly to the correct compliance manager with all relevant context attached.

Keep models private. Don’t run sensitive financial data through shared public APIs. Mask customer data before it touches any model. Validate outputs for anything involving financial advice or account details. Log every model interaction for audit purposes. And keep human escalation paths open for any query that involves sensitive account information.

Fraud detection pays off fastest as you are measuring against an existing fraud loss baseline, so the improvement is visible almost immediately. Document automation is close behind because the labor cost displacement is easy to calculate. Lending underwriting takes longer to validate because you need enough loan data over time to confirm the model’s accuracy, but the long-term returns tend to be the highest.

JPMorgan’s nearly $1.5 billion in AI-related savings came from stacking AI across multiple functions simultaneously, fraud, trading, document processing, credit. Bank of America’s Erica ROI is primarily call center deflection: every query Erica handles costs a fraction of a live agent interaction. Wells Fargo and Citi have made 80+ AI venture investments each since 2019, building capabilities ahead of the market.

The most common challenges include regulatory compliance, data privacy, explainability requirements, integrating with legacy systems, and maintaining appropriate human oversight for high-risk decisions.